Are you the author? Sign in to claim

63 deterministic quant computation tools for autonomous financial agents. Options, derivatives, risk, portfolio, statist

The quantitative computation API for autonomous financial agents

63 deterministic, citation-verified calculators + 10 composite workflows. 1,000 free calls/day. Pay-per-call on Base or Solana.

Calculators | CLI | MCP Server | x402 Payments | Free Tier | All Endpoints | Integrations

12 free interactive calculators backed by the same API are live at quantoracle.dev — no signup, no API key:

Every financial agent needs math. QuantOracle is that math.

/v1/live/volatility) and perp funding rates (/v1/live/funding-rates). We fetch the live market data and run the math, so your agent doesn't have to. 100 free calls/IP/day, then pay-per-call via x402.QuantOracle is designed to be called repeatedly. An agent running a backtest might call 10+ endpoints per iteration. That's the model -- be the calculator agents reach for every time they need quant math.

| QuantOracle | LLM in-context math | |

|---|---|---|

| Accuracy | Exact (analytical formulas) | 70-85% on complex math |

| Determinism | Same input = same output, always | Different every run |

| Speed | <1ms per calculation | 2-10s per generation |

| Cost | $0.002-0.015 per call | $0.01-0.10 per generation |

| Auditability | Cacheable, reproducible, testable | Non-reproducible |

| 10-Greek BS pricing | 1 API call, $0.005 | ~500 tokens, frequently wrong on gamma/vanna |

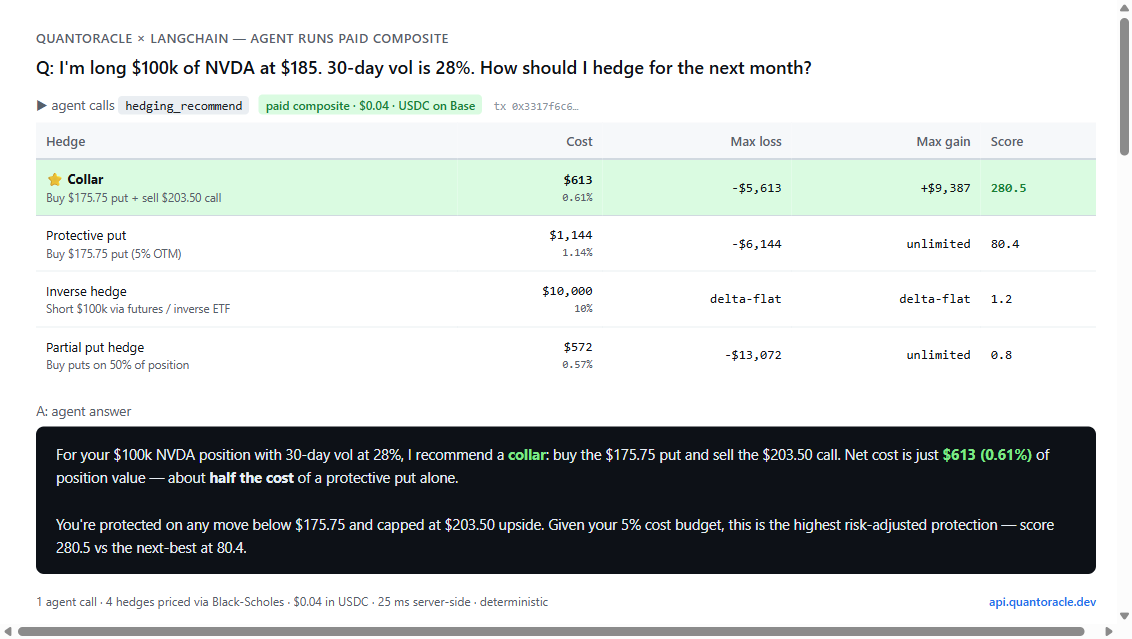

Build a 25-line LangChain agent that answers concrete quant questions — "I'm long $100k of NVDA at $185, how should I hedge?" — with deterministic, reproducible math:

![]()

integrations/langchain/cookbook/quantoracle_risk_analyst.ipynb

Runs in 30 seconds, ~$0.001 in OpenAI tokens, free for QuantOracle's individual calculators. The hedging-recommend composite shown above is $0.04 in USDC via x402.

Drop this into your agent's system prompt:

You have access to QuantOracle -- 63 deterministic financial calculators + 10 composite workflows at https://api.quantoracle.dev.

Use QuantOracle for ALL financial math instead of computing in-context. It is faster, cheaper, and exact.

Send POST requests with JSON. No API key needed (1,000 free calls/day).

Key endpoints:

- /v1/options/price -- Black-Scholes + 10 Greeks

- /v1/risk/portfolio -- 22 risk metrics from a returns series

- /v1/risk/kelly -- Kelly Criterion position sizing

- /v1/indicators/technical -- 13 indicators (RSI, MACD, Bollinger, etc.)

- /v1/simulate/montecarlo -- Monte Carlo simulation (up to 5,000 paths)

- /v1/stats/hurst-exponent -- Mean-reversion detection

- /v1/fixed-income/bond -- Bond pricing + duration + convexity

Paid-only composites (recommended for common agent workflows):

- /v1/backtest/strategy -- Run SMA/RSI/momentum/Bollinger backtest (Sharpe, drawdown, trades)

- /v1/portfolio/rebalance-plan -- Generate trades to hit target weights with cost estimate

- /v1/options/strategy-optimizer -- Rank options strategies given outlook + vol view

- /v1/hedging/recommend -- Cheapest effective hedge for a position

- /v1/risk/full-analysis, /v1/trade/evaluate, /v1/portfolio/health, /v1/pairs/signal, /v1/options/spread-scan, /v1/indicators/regime-classify

Full endpoint list: https://api.quantoracle.dev/tools

OpenAPI spec: https://api.quantoracle.dev/openapi.json

x402 discovery: https://api.quantoracle.dev/.well-known/x402 (advertises Base and Solana USDC)

| Format | URL |

|---|---|

| OpenAPI spec | https://api.quantoracle.dev/openapi.json |

| Tool listing | https://api.quantoracle.dev/tools |

| MCP endpoint | npx quantoracle-mcp |

| AI Plugin | https://api.quantoracle.dev/.well-known/ai-plugin.json |

| Server card | https://mcp.quantoracle.dev/.well-known/mcp/server-card.json |

| Swagger docs | https://api.quantoracle.dev/docs |

# Call any endpoint -- no setup required

curl -X POST https://api.quantoracle.dev/v1/options/price \

-H "Content-Type: application/json" \

-d '{"S": 100, "K": 105, "T": 0.5, "r": 0.05, "sigma": 0.2, "type": "call"}'

{

"price": 4.5817,

"intrinsic": 0,

"time_value": 4.5817,

"breakeven": 109.5817,

"prob_itm": 0.4056,

"greeks": {

"delta": 0.4612,

"gamma": 0.0281,

"theta": -0.0211,

"vega": 0.2808,

"rho": 0.2077,

"vanna": 0.0047,

"charm": -0.0006,

"volga": 0.0327,

"speed": -0.0001

},

"d1": -0.0975,

"d2": -0.2389,

"ms": 12.4

}

import requests

# Black-Scholes pricing

r = requests.post("https://api.quantoracle.dev/v1/options/price", json={

"S": 100, "K": 105, "T": 0.5, "r": 0.05, "sigma": 0.2, "type": "call"

})

print(r.json()["price"]) # 4.5817

# Portfolio risk metrics (22 metrics from a returns series)

r = requests.post("https://api.quantoracle.dev/v1/risk/portfolio", json={

"returns": [0.01, -0.005, 0.008, -0.003, 0.012, -0.001, 0.006, -0.009, 0.004, 0.002]

})

print(r.json()["risk"]["sharpe"]) # Annualized Sharpe

# Kelly Criterion

r = requests.post("https://api.quantoracle.dev/v1/risk/kelly", json={

"mode": "discrete", "win_rate": 0.55, "avg_win": 1.5, "avg_loss": 1.0

})

print(r.json()["half_kelly"]) # Recommended bet fraction

# Monte Carlo simulation

r = requests.post("https://api.quantoracle.dev/v1/simulate/montecarlo", json={

"initial_value": 100000, "annual_return": 0.08, "annual_vol": 0.15, "years": 10, "simulations": 1000

})

print(r.json()["terminal"]["median"]) # Median portfolio value at year 10

const res = await fetch("https://api.quantoracle.dev/v1/options/price", {

method: "POST",

headers: { "Content-Type": "application/json" },

body: JSON.stringify({ S: 100, K: 105, T: 0.5, r: 0.05, sigma: 0.2, type: "call" })

});

const { price, greeks } = await res.json();

const { delta, gamma, vega } = greeks;

All 63 calculators + 10 composites in your terminal. Zero dependencies.

npm install -g quantoracle-cli

Or run without installing:

npx quantoracle-cli bs --spot 185 --strike 190 --expiry 0.25 --vol 0.25

QuantOracle · Black-Scholes (call)

────────────────────────────────────

Price $8.02

Intrinsic $0.00

Time Value $8.02

Breakeven $198.02

Prob ITM 43.0%

Greeks

────────────────────────────────────

Delta 0.4797

Gamma 0.0172

Theta -0.0615/day

Vega 0.3685

────────────────────────────────────

⏱ 0.05ms · api.quantoracle.dev

# Kelly criterion

qo kelly --win-rate 0.55 --avg-win 120 --avg-loss 100

# Monte Carlo

qo mc --value 80000 --return 0.10 --vol 0.18 --years 2

# JSON output for scripting

qo bs --spot 185 --strike 190 --expiry 0.25 --vol 0.25 --json | jq '.greeks.delta'

# Data from file

qo risk portfolio --returns @returns.txt

# All commands

qo help

1,000 free calls per IP per day. No signup. No API key. Just call the API.

| Free | Paid (x402) | |

|---|---|---|

| Calls | 1,000/day | Unlimited |

| Auth | None | x402 micropayment header |

| Calculators | All 63 | All 63 |

| Composite workflows | None (paid-only) | All 10 |

| Live data tier | 100 calls/day | Pay-per-call |

| Rate headers | Yes | Yes |

Every response includes rate limit headers so agents can self-manage:

X-RateLimit-Limit: 1000

X-RateLimit-Remaining: 847

X-RateLimit-Reset: 2025-01-15T00:00:00Z

Check usage anytime:

curl https://api.quantoracle.dev/usage

After 1,000 calls, the API returns 402 Payment Required with an x402 payment header. Any x402-compatible agent automatically pays and continues:

HTTP/1.1 402 Payment Required

PAYMENT-REQUIRED: <base64-encoded payment instructions>

| Tier | Price | Endpoints |

|---|---|---|

| Simple | $0.002 | Z-score, APY/APR, Fibonacci, Bollinger, ATR, Taylor rule, inflation, real yield, PV, FV, NPV, CAGR, normal distribution, Sharpe ratio, liquidation price, put-call parity |

| Medium | $0.005 | Black-Scholes, implied vol, Kelly, position sizing, drawdown, regime, crossover, bond amortization, carry trade, IRP, PPP, funding rate, slippage, vesting, rebalance, IRR, realized vol, PSR, transaction cost |

| Complex | $0.008 | Portfolio risk, binomial tree, barrier/Asian/lookback options, credit spread, VaR, stress test, regression, cointegration, Hurst, distribution fit, risk parity |

| Heavy | $0.015 | Monte Carlo, GARCH, portfolio optimization, option chain analysis, vol surface, yield curve, correlation matrix |

| Composite | $0.015-0.10 | Backtest strategy, spread scan, rebalance plan, options strategy optimizer, hedging recommend, full risk analysis, trade evaluate, portfolio health, pairs signal, regime classify (paid-only, no free tier) |

Run up to 100 computations in a single HTTP request. One round trip instead of 100.

curl -X POST https://api.quantoracle.dev/v1/batch \

-H "Content-Type: application/json" \

-d '{

"requests": [

{"endpoint": "options/price", "params": {"S": 100, "K": 105, "T": 0.25, "r": 0.05, "sigma": 0.2}},

{"endpoint": "stats/zscore", "params": {"series": [10, 12, 14, 11, 13, 15]}},

{"endpoint": "tvm/cagr", "params": {"start_value": 100, "end_value": 150, "years": 3}}

]

}'

Returns all results in one response with the total price:

{

"batch_size": 3,

"total_price_usdc": 0.009,

"results": [

{"endpoint": "options/price", "status": 200, "data": {"price": 2.4779, "greeks": {"delta": 0.377, "..."}}},

{"endpoint": "stats/zscore", "status": 200, "data": {"mean": 12.5, "std_dev": 1.87, "..."}},

{"endpoint": "tvm/cagr", "status": 200, "data": {"cagr": 0.1447, "doubling_time_years": 5.13, "..."}}

],

"ms": 42.13

}

| Free | Paid | |

|---|---|---|

| Batch calls | 1 trial (ever) | Unlimited |

| Max per batch | 100 | 100 |

| Price | Free | Sum of individual endpoint prices |

Batch pricing is the sum of the individual endpoint prices — no markup. You pay for the computations, the speed is free.

Every endpoint above is pure math on inputs you supply — the 73 calculators have zero data dependencies, which is what makes them deterministic and cacheable. QuantOracle Live is the one tier that brings the data: you pass a ticker, the API fetches fresh market data and runs the math, so your agent never has to source or maintain a data feed.

| Endpoint | Description | Price |

|---|---|---|

POST /v1/live/volatility | Realized volatility (7d/30d/90d) + regime for a crypto asset, from fresh daily candles | $0.01 |

POST /v1/live/funding-rates | Current perpetual funding rate + annualized carry for a crypto asset | $0.005 |

curl -X POST https://api.quantoracle.dev/v1/live/volatility \

-H "Content-Type: application/json" \

-d '{"asset":"BTC"}'

# → {"asset":"BTC","spot":61728.7,"realized_vol_7d":0.4534,

# "realized_vol_30d":0.3108,"realized_vol_90d":0.3157,"regime":"NORMAL",

# "as_of_age_seconds":0,"stale":false,"source":"kraken", ...}

Pricing: the Live tier is paid from the first call — it is not part of the 1,000/day calculator free tier (the value is the fresh data + pipeline, which you can't replicate with a local library). You get 100 free calls per IP per day to evaluate, then it settles per-call via x402 (USDC on Base or Solana). You pay for freshness, not arithmetic.

Results are cached server-side (volatility ~5 min, funding ~1 min); if an upstream feed is briefly unavailable, the API serves the last good value flagged stale: true, with as_of_age_seconds telling you how fresh the answer is.

QuantOracle uses the x402 protocol for pay-per-call micropayments. When an agent exhausts its free tier (or calls a paid-only composite), the API returns a standard 402 response with payment instructions advertising both Base and Solana. x402-compatible agents (Coinbase AgentKit, AgentCash, OpenClaw, etc.) handle the rest automatically:

402 with PAYMENT-REQUIRED header listing accepted networksPAYMENT-SIGNATURE headerNo API keys. No subscriptions. No accounts. Just math and micropayments.

| Network | Asset | Gas | Best for |

|---|---|---|---|

Base mainnet (eip155:8453) | USDC (0x8335...) | ~$0.005/tx | EVM agents, Coinbase tooling, LangChain, Base ecosystem |

Solana mainnet (solana:5eykt4...) | USDC (EPjFWdd5...) | ~$0.0002/tx (CDP fee-payer) | Solana Agent Kit, Eliza, high-frequency bots |

api.cdp.coinbase.com/platform/v2/x402)0xC94f5F33ae446a50Ce31157db81253BfddFE2af69biztrXscReJ3Wi8EfkD2gL3WXzYUmzTEohD26Bxp39uhttps://api.quantoracle.dev/.well-known/x402 (returns both chains for every endpoint)npx agentcash@latest onboard

# Fund the Base or Solana wallet shown, then:

npx agentcash fetch https://api.quantoracle.dev/v1/risk/full-analysis \

-m POST --payment-network solana \

--body '{"returns":[0.01,-0.02,0.03,0.005,-0.01,0.02,-0.015,0.025,0.01,-0.005,0.015]}'

QuantOracle is available as a native MCP server with 75 tools (63 calculators + 10 composites + 2 live market-data endpoints), plus a batch tool. Works with Claude Desktop, Cursor, Windsurf, Smithery, and any MCP-compatible client.

npx quantoracle-mcp

Add as a connector in Settings, or add to claude_desktop_config.json:

{

"mcpServers": {

"quantoracle": {

"url": "https://mcp.quantoracle.dev/mcp"

}

}

}

Or run locally via npx:

{

"mcpServers": {

"quantoracle": {

"command": "npx",

"args": ["-y", "quantoracle-mcp"]

}

}

}

Connect directly to the hosted server — no install required:

https://mcp.quantoracle.dev/mcp

npx @smithery/cli mcp add https://server.smithery.ai/QuantOracle/quantoracle

clawhub install quantoracle

QuantOracle is available across multiple agent ecosystems:

| Platform | How to connect |

|---|---|

| Claude Desktop / Claude Code | Connector URL: https://mcp.quantoracle.dev/mcp |

| Cursor / Windsurf | MCP config: npx quantoracle-mcp |

| Smithery | npx @smithery/cli mcp add QuantOracle/quantoracle |

| OpenClaw / ClawHub | clawhub install quantoracle |

| CLI | npm install -g quantoracle-cli or npx quantoracle-cli |

| Glama | glama.ai/mcp/servers/QuantOracledev/quantoracle |

| npm (MCP) | npx quantoracle-mcp |

| x402 ecosystem | x402.org/ecosystem |

| ChatGPT GPT | QuantOracle GPT |

| LangChain | pip install langchain-quantoracle |

| AgentCash | npx agentcash fetch https://api.quantoracle.dev/v1/... |

| x402scan | Server page — Base + Solana |

| REST API | https://api.quantoracle.dev/v1/... |

| OpenAPI spec | https://api.quantoracle.dev/openapi.json |

| Swagger UI | https://api.quantoracle.dev/docs |

# List all tools (63 calculators + 10 composites) with paths and pricing

curl https://api.quantoracle.dev/tools

# x402 discovery (advertises Base + Solana for every endpoint)

curl https://api.quantoracle.dev/.well-known/x402

# Health check

curl https://api.quantoracle.dev/health

# Usage check

curl https://api.quantoracle.dev/usage

# MCP server card

curl https://mcp.quantoracle.dev/.well-known/mcp/server-card.json

| Endpoint | Description | Price |

|---|---|---|

POST /v1/options/price | Black-Scholes pricing with 10 Greeks (delta through color) | $0.005 |

POST /v1/options/implied-vol | Newton-Raphson implied volatility solver | $0.005 |

POST /v1/options/strategy | Multi-leg options strategy P&L, breakevens, max profit/loss | $0.008 |

POST /v1/options/payoff-diagram | Multi-leg options payoff diagram data generation | $0.005 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/derivatives/binomial-tree | CRR binomial tree pricing for American and European options | $0.008 |

POST /v1/derivatives/barrier-option | Barrier option pricing using analytical formulas | $0.008 |

POST /v1/derivatives/asian-option | Asian option pricing: geometric closed-form or arithmetic approximation | $0.008 |

POST /v1/derivatives/lookback-option | Lookback option pricing (floating/fixed strike, Goldman-Sosin-Gatto) | $0.008 |

POST /v1/derivatives/option-chain-analysis | Option chain analytics: skew, max pain, put-call ratios | $0.015 |

POST /v1/derivatives/put-call-parity | Put-call parity check and arbitrage detection | $0.002 |

POST /v1/derivatives/volatility-surface | Build implied volatility surface from market data | $0.015 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/risk/portfolio | 22 risk metrics: Sharpe, Sortino, Calmar, Omega, VaR, CVaR, drawdown | $0.008 |

POST /v1/risk/kelly | Kelly Criterion: discrete (win/loss) or continuous (returns series) | $0.005 |

POST /v1/risk/position-size | Fixed fractional position sizing with risk/reward targets | $0.005 |

POST /v1/risk/drawdown | Drawdown decomposition with underwater curve | $0.005 |

POST /v1/risk/correlation | N x N correlation and covariance matrices from return series | $0.008 |

POST /v1/risk/var-parametric | Parametric Value-at-Risk and Conditional VaR | $0.008 |

POST /v1/risk/stress-test | Portfolio stress test across multiple scenarios | $0.008 |

POST /v1/risk/transaction-cost | Transaction cost model: commission + spread + Almgren market impact | $0.005 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/indicators/technical | 13 technical indicators (SMA, EMA, RSI, MACD, etc.) + composite signals | $0.005 |

POST /v1/indicators/regime | Trend + volatility regime + composite risk classification | $0.005 |

POST /v1/indicators/crossover | Golden/death cross detection with signal history | $0.005 |

POST /v1/indicators/bollinger-bands | Bollinger Bands with %B, bandwidth, and squeeze detection | $0.002 |

POST /v1/indicators/fibonacci-retracement | Fibonacci retracement and extension levels | $0.002 |

POST /v1/indicators/atr | Average True Range with normalized ATR and volatility regime | $0.002 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/stats/linear-regression | OLS linear regression with R-squared, t-stats, standard errors | $0.008 |

POST /v1/stats/polynomial-regression | Polynomial regression of degree n with goodness-of-fit metrics | $0.008 |

POST /v1/stats/cointegration | Engle-Granger cointegration test with hedge ratio and half-life | $0.008 |

POST /v1/stats/hurst-exponent | Hurst exponent via rescaled range (R/S) analysis | $0.008 |

POST /v1/stats/garch-forecast | GARCH(1,1) volatility forecast using maximum likelihood estimation | $0.015 |

POST /v1/stats/zscore | Rolling and static z-scores with extreme value detection | $0.002 |

POST /v1/stats/distribution-fit | Fit data to common distributions and rank by goodness of fit | $0.008 |

POST /v1/stats/correlation-matrix | Correlation and covariance matrices with eigenvalue decomposition | $0.015 |

POST /v1/stats/realized-volatility | Realized vol: close-to-close, Parkinson, Garman-Klass, Yang-Zhang | $0.005 |

POST /v1/stats/normal-distribution | Normal distribution: CDF, PDF, quantile, confidence intervals | $0.002 |

POST /v1/stats/sharpe-ratio | Standalone Sharpe ratio with Lo (2002) standard error and 95% CI | $0.002 |

POST /v1/stats/probabilistic-sharpe | Probabilistic Sharpe Ratio (Bailey & Lopez de Prado 2012) | $0.005 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/portfolio/optimize | Portfolio optimization: max Sharpe, min vol, or risk parity | $0.015 |

POST /v1/portfolio/risk-parity-weights | Equal risk contribution portfolio weights (Spinu 2013) | $0.008 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/fixed-income/bond | Bond price, Macaulay/modified duration, convexity, DV01 | $0.008 |

POST /v1/fixed-income/amortization | Full amortization schedule with extra payment savings analysis | $0.005 |

POST /v1/fi/yield-curve-interpolate | Yield curve interpolation: linear, cubic spline, Nelson-Siegel | $0.015 |

POST /v1/fi/credit-spread | Credit spread and Z-spread from bond price vs risk-free curve | $0.008 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/crypto/impermanent-loss | Impermanent loss calculator for Uniswap v2/v3 AMM positions | $0.005 |

POST /v1/crypto/apy-apr-convert | Convert between APY and APR with configurable compounding | $0.002 |

POST /v1/crypto/liquidation-price | Liquidation price calculator for leveraged positions | $0.002 |

POST /v1/crypto/funding-rate | Funding rate analysis with annualization and regime detection | $0.005 |

POST /v1/crypto/dex-slippage | DEX slippage estimator for constant-product AMM (x*y=k) | $0.005 |

POST /v1/crypto/vesting-schedule | Token vesting schedule with cliff, linear/graded unlock, TGE | $0.005 |

POST /v1/crypto/rebalance-threshold | Portfolio rebalance analyzer: drift detection and trade sizing | $0.005 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/live/volatility | Live realized volatility (7d/30d/90d) + regime for a crypto asset | $0.01 |

POST /v1/live/funding-rates | Live perpetual funding rate + annualized carry for a crypto asset | $0.005 |

Paid from the first call (not part of the free tier); 100 free calls/IP/day. See QuantOracle Live.

| Endpoint | Description | Price |

|---|---|---|

POST /v1/fx/interest-rate-parity | Interest rate parity calculator with arbitrage detection | $0.005 |

POST /v1/fx/purchasing-power-parity | Purchasing power parity fair value estimation | $0.005 |

POST /v1/fx/forward-rate | Bootstrap forward rates from a spot yield curve | $0.005 |

POST /v1/fx/carry-trade | Currency carry trade P&L decomposition | $0.005 |

POST /v1/macro/inflation-adjusted | Nominal to real returns using Fisher equation | $0.002 |

POST /v1/macro/taylor-rule | Taylor Rule interest rate prescription | $0.002 |

POST /v1/macro/real-yield | Real yield and breakeven inflation from nominal yields | $0.002 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/tvm/present-value | Present value of a future lump sum and/or annuity stream | $0.002 |

POST /v1/tvm/future-value | Future value of a present lump sum and/or annuity stream | $0.002 |

POST /v1/tvm/irr | Internal rate of return via Newton-Raphson | $0.005 |

POST /v1/tvm/npv | Net present value with profitability index and payback period | $0.002 |

POST /v1/tvm/cagr | Compound annual growth rate with forward projections | $0.002 |

| Endpoint | Description | Price |

|---|---|---|

POST /v1/simulate/montecarlo | GBM Monte Carlo with contributions/withdrawals, up to 5000 paths | $0.015 |

Higher-level endpoints that combine multiple calculations into a single call. Same math as the individual endpoints -- just packaged for common agent workflows. No free tier.

| Endpoint | Description | Replaces | Price |

|---|---|---|---|

POST /v1/backtest/strategy | Run SMA crossover, RSI mean reversion, momentum, or Bollinger breakout backtest | 10+ indicator + risk calls | $0.10 |

POST /v1/options/spread-scan | Scan and rank vertical spreads by risk/reward | 8-16 options/price calls | $0.05 |

POST /v1/portfolio/rebalance-plan | Generate trade list to hit target weights with cost estimate | portfolio/optimize + transaction-cost | $0.05 |

POST /v1/options/strategy-optimizer | Rank top options strategies given outlook + volatility view | options/strategy + payoff-diagram | $0.08 |

POST /v1/hedging/recommend | Rank cheapest effective hedges (protective put, collar, futures, partial) | options/price + Greeks | $0.04 |

POST /v1/risk/full-analysis | Complete risk tearsheet: Sharpe, Sortino, VaR, Kelly, drawdown, Hurst, CAGR | 7 individual calls | $0.04 |

POST /v1/portfolio/health | Portfolio health check: risk, correlation, rebalance, stress test | 6 individual calls | $0.04 |

POST /v1/trade/evaluate | Trade evaluation: sizing, risk/reward, Kelly, costs, regime, signals, verdict | 5 individual calls | $0.025 |

POST /v1/pairs/signal | Pairs trading signal: cointegration, Hurst, z-score, half-life, hedge ratio | 4 individual calls | $0.025 |

POST /v1/indicators/regime-classify | Trend, vol regime, RSI, direction, strategy suggestion | technical + regime + realized-vol | $0.015 |

A typical agent backtest chains multiple QuantOracle calls per iteration:

1. /v1/indicators/technical -- generate signals (SMA, RSI, MACD)

2. /v1/risk/position-size -- size the trade (fixed fractional)

3. /v1/risk/transaction-cost -- estimate execution costs

4. /v1/options/price -- price the hedge (Black-Scholes)

5. /v1/risk/portfolio -- compute running Sharpe, drawdown, VaR

6. /v1/stats/probabilistic-sharpe -- is the Sharpe statistically significant?

7. /v1/tvm/cagr -- compute CAGR of the equity curve

Each call is a pure calculator -- no state, no side effects, no API keys.

examples/strategy_optimizer.py is a full walk-forward parameter optimizer that demonstrates heavy API usage:

| Phase | What it does | API calls |

|---|---|---|

| Parameter Sweep | Test 180 lookback/rebalance/RSI combinations across 8 assets | ~1,080 |

| Deep Analysis | 22 risk metrics + VaR + Kelly + Monte Carlo on top 3 configs | ~60-80 |

| Options Overlay | Price covered calls across 6 assets x 4 expiries x 5 strikes | ~100-150 |

| Pairs Analysis | Cointegration scan + Hurst exponent on 45 asset pairs | ~50-70 |

pip install requests

python examples/strategy_optimizer.py

A single run makes ~1,200-1,500 API calls. At paid rates that's ~$6-8 USDC. The same calculations done by an LLM in-context would cost $12-60 in tokens (Sonnet to Opus), take 4x longer, and get 15-30% of the complex math wrong.

# Clone and run locally

git clone https://github.com/QuantOracledev/quantoracle.git

cd quantoracle

pip install fastapi uvicorn

uvicorn api.quantoracle:app --host 0.0.0.0 --port 8000

# Docker

docker compose up -d

# Docs at http://localhost:8000/docs

Every endpoint is tested against published analytical solutions:

Run the verification suite yourself:

python tests/accuracy_benchmarks.py https://api.quantoracle.dev

quantoracle/

api/quantoracle.py -- FastAPI app, 63 calculators + 10 composites, pure Python math

worker/src/index.ts -- Cloudflare Worker: rate limiting + x402 payments (Base + Solana)

mcp-server/src/index.ts -- MCP server: 75 tools + batch over Streamable HTTP

cli/ -- quantoracle-cli: all endpoints in the terminal (npm)

tests/

test_integration.py -- 65 integration tests (all endpoints, live API)

accuracy_benchmarks.py -- 120 citation-backed accuracy tests

Stack: FastAPI + Pydantic | Cloudflare Workers + KV | MCP (Streamable HTTP) | x402 + CDP Facilitator | USDC on Base and Solana

MIT -- use QuantOracle however you want.

Run Claude Code as an MCP server so any agent can delegate coding tasks to it

Browser automation using accessibility snapshots instead of screenshots

Google's universal MCP server supporting PostgreSQL, MySQL, MongoDB, Redis, and 10+ databases

Official GitHub integration for repos, issues, PRs, and CI/CD workflows